Running a successful restaurant requires more than just culinary skills and a knack for hospitality. Restaurants have the highest rates of failure for new businesses, that is right, they are #1. Effective financial management, specifically restaurant accounting, is a key component for maintaining profitability, understanding, and sustainability. Unfortunately, many restaurant owners and managers trust themselves or an underpaid accountant who make common accounting mistakes that can lead to financial pitfalls. In this article, we'll explore some of these mistakes and offer practical solutions to help you steer clear of them.

One of the most fundamental aspects of restaurant accounting is maintaining accurate and up-to-date records. This includes tracking all income and expenses, maintaining detailed receipts, and documenting all financial transactions. Neglecting this crucial task can lead to discrepancies, missed deductions, and inaccurate financial reports. Solution: Implement a reliable accounting system for your restaurant. Use

accounting software that you also have access to. The goal here is to automate and streamline record-keeping processes. Also remember to regularly reconcile accounts to ensure accuracy. Our firm utilizes QuickBooks Online as a way to not only complete the majority of the accounting process on our own but also to create an easy access point for our clients to view their own financial records.

A common mistake among small restaurant owners is mixing personal and business finances. This can lead to confusion, tax issues, and difficulty in tracking the financial health of the restaurant.

Solution: Open separate bank accounts and credit cards for your restaurant. Ensure all business transactions are conducted through these accounts to maintain clear boundaries between personal and business finances. We recommend utilizing Relay Financial as a software which allows you to separate and have better control over how your money is managed and spent.

Cash flow is the lifeblood of any restaurant. Poor cash flow management can result in an inability to pay suppliers, staff, and other operational costs, leading to potential closure.

Solution: Regularly monitor your cash flow, especially for distributors. Create cash flow forecasts to anticipate future financial needs and identify potential shortfalls. Implement practices such as managing inventory efficiently, negotiating better payment terms with suppliers, and optimizing labor costs. A large portion of this is managing your tax liabilities through estimated payments. Unfortunately, this is the highest failure risk for small business and is often unmanaged, as we will talk about later.

Inventory management is a critical component of restaurant accounting. Poor inventory practices can lead to overstocking, waste, and increased costs, ultimately affecting profitability.

Solution: Use inventory management software to track stock levels, monitor usage patterns, and reduce waste. Conduct regular physical inventory counts to ensure accuracy and adjust purchasing accordingly. This step requires a great deal of time and effort which is often undervalued by managers and owners. Keeping track of food walking out the backdoor and alcohol being overpoured is a long-term cost saver

Restaurants are subject to various taxes, including sales tax, payroll tax, and income tax. Ignoring these obligations can result in hefty fines, penalties, and legal issues.

Solution: Stay informed about the tax requirements specific to your location. Use accounting software that includes tax compliance features to track and remit taxes accurately and on time. This is where hiring an accounting firm for restaurants comes in the most handy.

Payroll is often one of the largest expenses for a restaurant. Inadequate payroll management can lead to issues such as overpayment, underpayment, and compliance violations.

Solution: Implement a robust payroll system that accurately tracks hours worked, overtime, and benefits. Ensure compliance with labor laws and regulations. Regularly review payroll reports for accuracy and make adjustments as necessary. Make sure you are separating back of house and front of house when analyzing payroll. Kitchen cost versus food income is a very important metric that needs to be performed throughout the year.

Without a proper budget and financial plan, restaurant owners can struggle to manage expenses and anticipate future financial needs. This can lead to overspending and financial instability.

Solution: Budgets are extremely helpful for making decisions and evaluating success. Creating a detailed budget that includes all expected income and expenses sets a goal for yourself to judge yourself on. Regularly review and adjust the budget based on actual performance. Develop a long-term financial plan that aligns with your business goals and objectives.

Accurate financial reporting is essential for understanding the financial health of your restaurant. Many restaurant owners fail to produce regular financial statements, leading to a lack of insight into profitability and performance.

Solution: Generate and review financial statements regularly, including income statements, balance sheets, and cash flow statements. These accounting reports can also be used to obtain loans which may be needed if you have large hopes for the future of the business. Use these reports to identify trends, track performance, and make informed business decisions.

Many restaurant owners try to manage their accounting without professional help, leading to errors and missed opportunities for financial optimization.

Solution: As a heavily biased solution, Blue Heron CPAs helps you with all of the above. We help our clients better than they can help themselves and we strive to inform customers on all of their restaurant accounting needs. Even with a professional, we see many mistakes that professionals make and that allows us to fix and create large profits for our customers. Blue Heron CPAs has spent years studying and researching how to best help restaurants with their accounting process.

Effective restaurant accounting is vital for the success and longevity of your business. By avoiding these common mistakes and implementing best practices, you can create accurate financial management, maintain profitability, and achieve your business goals. Remember, investing in the right tools, systems, and professional guidance can make a significant difference in the financial health of your restaurant.

Embrace these strategies to avoid common pitfalls in restaurant accounting, and you'll be well on your way to a thriving, financially sound restaurant business.

Selling your home can be a major life event. It's important to understand the federal tax implications before you put your house on the market. One of the biggest concerns for homeowners is how to minimize their federal tax liability when they sell their house.

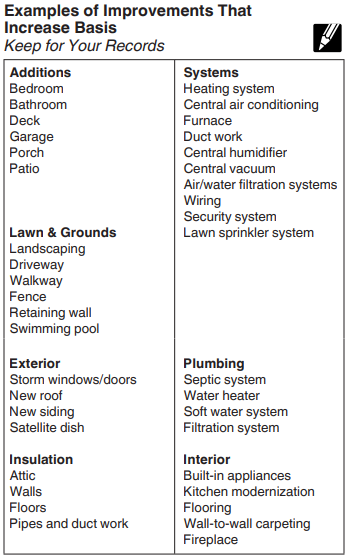

The Internal Revenue Service (IRS) plays an important role in the sale of your home. When you sell your home, you may be required to pay taxes on the capital gain. This is the difference between the sale price and your adjusted basis. (the purchase price plus any improvements you've made to the home, minus depreciation)

Minimizing your tax liability when selling your house takes careful planning and understanding of the applicable tax regulations.

By implementing these strategies and seeking professional guidance when needed, you can effectively minimize your tax liability when selling your house and maximize your financial gains.

In addition to the home sale exclusion, there are a number of other deductions that you may be able to claim when you sell your home. These deductions may include expenses related to selling your home, such as real estate commissions and closing costs. You may also be able to deduct certain home improvements that you made in the years leading up to the sale.

If you are selling your home, it is important to report the sale on your tax return. You will need to report the sale price of your home, your adjusted basis, and any capital gains or losses that you realized from the sale. You may also need to report any deductions that you are claiming related to the sale of your home. Selling your home can be a complex process, but it doesn't have to be overwhelming. By following these tips, you can ensure that you are reporting the sale of your home to the IRS correctly and minimizing your tax liability.

Selling your home can be a major life event, and it's important to understand the tax implications before you put your house on the market. One common question that homeowners have is whether or not they have to pay taxes on the sale of their home if they're over 65.

There are no current capital gains tax breaks based on age. If you meet certain requirements though, you may be able to exclude up to $250,000 ($500,000 if you're married filing jointly) of capital gains from the sale of your primary residence from your taxable income. However, there are some important exceptions to this rule.

To qualify for the home sale exclusion, you generally meet the following requirements:

If you meet these requirements, you may be able to exclude the capital gains from your taxable income, even if you have a significant gain on the sale of your home.

There are a few exceptions to the home sale exclusion. For example, you may not be able to exclude the gain from your taxable income if:

If you are considering selling your home, it is important to consult with a tax professional to determine whether or not you qualify for the home sale exclusion and to calculate your potential capital gain.

To calculate your capital gain from the sale of your home, you'll need to subtract your adjusted basis from your sales price. Your adjusted basis is the amount you paid for the home, plus any improvements you've made to the home, and selling expenses. There are additional increases to basis for a primary household but improvements are the most common and any previous depreciation is recaptured which is a different type of gain.

For example, let's say you purchased your home for $200,000 in 2010. You made $50,000 in improvements to the home over the years, and you claimed $10,000 in depreciation. Your adjusted basis would be $250,000 ($200,000 + $50,000). If you sell your home for $300,000, your capital gain would be $50,000 ($300,000 - $250,000) along with the $10,000 being recaptured. If you qualify for the home sale exclusion, you can exclude up to $250,000 of your capital gain from your taxable income.

It is important to note that your capital gain tax liability is calculated from the capital gain tax bracket. Be sure to consult with a tax professional to get an accurate estimate of your tax liability.

Source: Internal Revenue Service

Selling your home can be a big life event, and there are a few things you need to keep in mind when it comes to taxes. One important step is to report the sale of your home on your tax return.

To do this, you'll need to file Schedule D (Capital Gains and Losses). On Schedule D, you'll list the sales price of your home, your adjusted basis (which is the purchase price plus any improvements you've made to the home), and your capital gain (or loss).

There are many additional important facts about selling your house that may affect the treatment of any large transactions. Specifically for home sales, review IRS Publication 523 for the complete list of rules around selling your house.

There are a few things you can do to minimize your tax liability when selling your home, such as:

Whether or not you have to pay taxes on the sale of your home if you're over 65 depends on a number of factors, including whether you qualify for the home sale exclusion and how much capital gain you have. If you have any questions about the tax implications of selling your home, you should consult with a qualified tax professional.

Blue Heron CPAs often performs business consulting for those thinking about forming an S Corporation. There are many questions we ask that go far beyond the tax liability, like reasonable compensation. To ensure that an S Corporation is the right entity structure for our clients as it relates to taxes. Much of those questions relate to managing basis, paying yourself in an S Corporation, and the expected normal operations of the company. Understanding the consequences of making an S election is important.

This article identifies potential red flags that we commonly see in S Corporations. This article does not identify all errors or all issues we commonly see. This resource intends to help individuals educate themselves through proper communication with their tax preparers. Your tax preparer should be capable of having a conversation towards any of the below topics. This will help further qualify whether that preparer is the correct person for the service you are being provided.

Many small business owners form S Corporations to take advantage of significant tax benefits, especially those related to self-employment taxes. However, navigating the complexities of S Corporation operations can be challenging. Prior to electing an S Corporation, you should evaluate the complexities for whether you intend to comply with the law. In this blog article, we'll explore three common issue areas we see in S Corporations: reasonable compensation, managing your basis, and mileage for personal cars. Many tax preparers put the responsibility of compliance for these requirements on the taxpayer. Taxpayers are responsible for accurately and properly filing their tax returns and following the rules and regulations for their respective entities.

One of the most critical issues for S Corporation owners is paying yourself in an S Corporation, also known as "reasonable compensation." The IRS closely scrutinizes the salary that owners pay themselves. This prevents individuals from reducing their tax liability by paying too little in wages and taking the rest as distributions. Here are some key points to consider when paying yourself in an S Corporation:

Reasonable compensation is the salary an S Corporation owner or shareholder should pay themselves for their work within the business. There is no direct guidance on how to calculate reasonable compensation but the IRS guidance below discusses a potential calculation.

Proper documentation on how you came to your salary number is crucial. Maintain records of salary surveys, job descriptions, and any other information that supports the chosen salary level. This documentation is invaluable in case of an IRS audit.

Reasonable compensation is subject to payroll taxes (Social Security and Medicare), while distributions are not. Paying too little in salary can lead to IRS penalties and additional tax liabilities including their ability to classify past distributions as wages.

There are consequences to underpaying self-employment tax. When calculating a Social Security benefit during retirement, reduced wages can heavily reduce the future benefit you receive.

“I was reading into S Corporation requirements, and it mentions reasonable compensation as a requirement to operate as an S Corporation. Should I be on the company’s payroll and am I taking the proper amount of salary?”

To ensure compliance, it's advisable to consult with a tax professional. A professional can help determine a reasonable compensation level that aligns with IRS guidelines and industry standards.

Basis in an S Corporation is the investment that the shareholders have in the company. Like understanding the cost of what you put into a house when you sell it or stocks as you sell them, you have a basis in your company. The IRS requires taxpayers to track their basis, a crucial calculation for tax purposes. Basis may not affect your income and the taxes you owe every year which is why it is a hidden dagger that has severe tax consequences in future years.

Basis can increase through various means. I usually think of this as putting additional investment into the business.

Your company’s basis is recognized through Schedule M-2 which is located on Page 5 of the 1120-S. It is required for every S Corporation to track and report basis properly. On your individual return, a Form 7203 is likely filed to report the individuals basis within the S Corp.

Signs of basis mismanagement include the following common red flags. If you see any of the following, it is worth asking your accountant if your basis is accurately tracked and why it is reported this way. The below does not identify that a mistake has been made. It identifies that there is a high likelihood that you should talk to your accountant.

“I was reading into S Corporation requirements to manage your basis. I was hoping you might be able to explain the Schedule M-2 to me along with my Form 7203.”

To properly manage your basis, work closely with a tax professional who specializes in S Corporations. They can help you establish a basis tracking system, maintain accurate records, and ensure that you're compliant with IRS regulations.

Have you ever been advised by TikTok or a friend to title a new vehicle under the business because it becomes a tax deduction? Your friend might be right, but they are likely not explaining the entire story for how you must treat that vehicle for the future. S Corporation owners often use personal vehicles for business purposes. S Corporation owners also may use business vehicles for personal use. Keep in mind that shareholders who are actively working within the S Corporation are considered employees of the S Corporation. Properly handling vehicle expenses is essential for tax efficiency but also a requirement to the IRS which reduces tax liabilities. Here are some key considerations:

There is not great guidance specifically towards the topic of vehicles held in S Corporations. There are common mistakes around vehicle deductions through business vehicles titled in the business’ name.

I have been researching how to get the maximum amount of deduction for my business vehicle and I came across an article describing the mileage reimbursement for personal vehicles. Are we currently performing a reimbursement and are we claiming a deduction?

I hope this article is helpful to those who have trouble approaching tough conversations about accounting and taxes. It is important to remember that the taxpayer, you, is ultimately responsible for your tax return and the numbers included on that return.

S Corporations offer numerous advantages, but they also come with complexities that require careful attention. Understanding reasonable compensation, basis, and mileage reimbursement rules is crucial for maintaining compliance with tax regulations and optimizing your tax strategy. Consulting with tax professionals, keeping accurate records, and managing basis effectively will help you navigate these challenges successfully and maximize the benefits of your S Corporation structure.

In the busyness of our daily lives, it's easy to view tax season as just another to-do list item. For many, that means a quick rush to file taxes without a second thought. However, there's a hidden gem in the realm of financial responsibility that often goes overlooked: the tax return review. In this article, we'll explore why a tax return review is crucial for your financial well-being. Additionally, we will look at how it can help you maximize your financial potential. The best part of our services is that you do not need to switch your current tax preparer.

We're focused on providing information so that you can ask good questions and work towards getting an accurate tax return. Most tax preparers appreciate good questions as it also reduces their own liability if the tax return is done properly. The most important thing to understand, it is your responsibility as the taxpayer to have an accurate tax return. Tax preparers hold very little liability and it is the taxpayer’s responsibility to understand the tax return being filed.

Before delving into the importance of a tax return review, let's clarify what it entails. A tax return review involves a thorough look at your filed tax return by a Certified Public Accountant (CPA). This process goes beyond a cursory glance to identify potential errors, missed deductions, or opportunities for tax savings. It is intended to provide opportunities to minimize tax liabilities. It will also educate and inform you on your tax return, and reduce tax noncompliance where hidden errors are occurring.

The most important reason for getting your tax return reviewed is to educate yourself on what the tax return says. Through a quick explanation of what the tax return says, you can compare it to what you already know about your business. This comparison helps identify errors immediately but also helps reduce errors through your ability to understand the key points of a tax return.

Another primary reason for having your tax return reviewed is to catch any errors or omissions in your

filing. Even the most diligent taxpayers can make mistakes, and these errors can lead to costly penalties or audits. A professional review can help identify and rectify these issues before they escalate. Hidden mistakes from unintentional errors and omissions can bankrupt a company unexpectedly. Our focus is on improving your business’ financial health.

Tax laws are complex, and they change regularly. A tax professional is well-versed in these laws and can ensure that you are taking advantage of all available deductions and credits. This can result in significant tax savings that you might have otherwise missed.

Tax return reviews are not just about finding deductions; they are also about optimizing your overall tax

strategy. A tax professional can help structure your finances in a way that minimizes your tax liability, ensuring that you keep more of your hard-earned money.

IRS Tax audits can be stressful and time-consuming. By having your tax return reviewed, you reduce the risk of incurring a tax liability during the IRS audit due to inaccuracies or inconsistencies. Additionally, if you do face an audit, having a professionally reviewed tax return can help. The review can create and advise towards valuable documentation and support which may be forgotten later.

A tax return review can be a valuable part of your overall tax planning. It provides insights into your future tax health, highlights areas for improvement, and helps you make informed decisions about your future financial goals. Tax Planning is a crucial component in paying the least amount of taxes over your entire life. There are situations where paying the least amount of tax today, creates a large tax liability in the future which can be identified.

In the world of personal tax and finance, a tax return review is a powerful tool that should be regularly utilized. It serves as a safeguard against costly mistakes, a catalyst for maximizing your tax benefits, and a means of ensuring compliance with tax regulations. By investing in a tax return review, you not only protect your financial well-being but also pave the way for a more secure and prosperous financial future. Don't let tax season pass you by without taking advantage of this opportunity to achieve peace of mind and financial success. Trust in the expertise of professionals who can provide a thorough Tax Return Review, and watch as your financial potential unfolds before you.

As tax season approaches, one of the most critical decisions you'll make is choosing the right tax preparer who can navigate the complex world of taxation while ensuring your financial well-being. Not all tax professionals are created equal and attention to detail is the largest quality to the accuracy of your tax preparer. To help you make an informed choice, we've compiled a guide on essential certifications and qualifications you should be looking for when finding and qualifying a tax preparer.

Anyone with an IRS Preparer Tax Identification Number (PTIN) is authorized to prepare federal tax returns. To obtain a Preparer Tax Identification Number (PTIN), individuals must go through a quick registration process with the IRS. However, the qualifications necessary to identify yourself as a tax preparer are very low and there are no educational requirements.

Based on demand and the ability to easily set up a business, many seasonal tax firms pop up around Florida. Seasonal tax preparers are often hired temporarily during tax season to handle the influx of returns. They may not always possess the necessary credentials, making them more susceptible to becoming ghost preparers. It's crucial for taxpayers to exercise caution when seeking assistance from such preparers. Even though some seasonal preparers may be legitimate and have the requisite skills, it's essential to verify their qualifications. You should ask for their PTIN, and ensure they are associated with a reputable tax preparation service or organization. Being diligent in your selection process can help you avoid the potential pitfalls associated with ghost preparers and ensure that your tax return is handled accurately and ethically.

Typically, looking for an accounting firm is a good way to avoid unqualified tax preparers. Each state also has their own requirements for marketing and the naming of an accounting firm. In Texas, the law does not allow you to identify as an Accountant in your name unless you hold a Certified Public Accountant License. In Florida, there are very few rules when starting an accounting firm and there are very few restrictions on what you can name a business. Thus, a person with no qualification can start an accounting firm tomorrow within Florida.

If you are specifically looking for a certified individual to perform your work. Looking for a business with “CPAs” within its name is important. CPA firms must have the majority of their ownership owned by a CPA. The reason why the “s” is so important is that it indicates multiple CPAs are involved within the ownership. Firms with multiple certified individuals perform better as the firm is less likely to rely on one person to make decisions. This increases the ability of the firm to prepare an accurate return and also typically reflects a larger amount of knowledge in the firm. If you do not require a CPA firm to perform your work, it is much harder to qualify a preparer for your tax return through the business’ name.

There are many important qualities to think about when choosing a tax preparer. The most important one is whether the preparer has the ability to defend their work in front of the IRS. You will find this quality important if you receive an IRS Audit letter in the future. If your preparer is not able to defend each step of an IRS Audit, you will need to involve additional individuals which may cost substantially more in your defense.

Enrolled Agents are tax experts licensed by the IRS. They must pass a three-part exam, demonstrating proficiency in federal tax planning, individual and business tax return preparation, and representation. EAs are required to complete 72 hours of continuing education every three years. Enrolled Agents are certified in Tax services which includes portions of accounting. The certification’s tests focus on tax compliance and tax return preparation for individuals and businesses. Typical services performed by Enrolled Agents include tax preparation, tax planning, IRS Representation, and many other tax related services.

CPAs are licensed by state boards of accountancy. They have passed the Uniform CPA Examination, which is a 4 part exam. CPAs have taken 150 hours of college credit, much of which must be high level accounting courses, and typically have a Bachelor’s degree. CPAs also must meet experience and ethical requirements and engage in ongoing continuing education to maintain their CPA license. The CPA license is intended to be the most broad and prestigious license in Accounting.

The Uniform CPA Examination is known to be one of the hardest exams to pass. By identifying a CPA as your preferred tax preparer certification, you are guaranteeing a well-rounded accountant is preparing your return. Each part of the 4 part exam has a pass rate around 50% along with an average study period of over 12 months. Therefore, utilizing a CPA for your tax preparation is considered to be the safest option if you are qualifying a tax preparer by their certification.

In regards to tax preparation, not every CPA has the knowledge to perform tax preparation well. Qualifying that the CPA has a focus on tax preparation and tax strategies is a good idea when looking for a tax preparer. Typical services performed by a CPA include all tax services, accounting services, advisory and audit services, along with almost every other service in accounting. Just keep in mind that CPAs should not identify as being good at all services and typically have a specialization such as tax return preparation.

Attorneys are licensed by state courts or their designees, such as the state bar. They have earned a degree in law and passed a bar exam. Attorneys are held to high ethical standards and must participate in ongoing continuing education. Most attorneys performing tax preparation are tax attorneys. Tax attorneys typically have extensive and specialized knowledge in accounting and tax.

Tax preparers without the above-mentioned credentials, have limited practice rights. They can only represent clients before specific IRS employees but not in appeals or collection issues. These preparers include:

To assist taxpayers in determining the credentials and qualifications of tax professionals, the IRS maintains a public directory. This searchable database includes the names, locations, and credentials of attorneys, CPAs, enrolled agents, enrolled retirement plan agents, and enrolled actuaries with valid PTINs, as well as Annual Filing Season Program Record of Completion recipients for the current tax year.

It is crucial to ensure that your tax preparer holds the necessary credentials and qualifications to handle your financial affairs effectively. For this reason, always verify that your tax preparer has an IRS-issued PTIN, which is required by law for anyone who prepares tax returns for compensation. When selecting a tax professional, inquire about their education, training, and experience to make an informed choice. Your financial well-being depends on it, so choose wisely and with confidence.

If you consistently owe taxes at the end of the year when filing your Form 1040 (U.S. Individual Income Tax Return), there are several common reasons why this might be happening. Understanding these reasons can help you take steps to better manage your tax liability. Here are some potential explanations for consistently owing taxes:

One of the most common reasons for owing taxes at the end of the year is that your income sources did not withhold enough federal tax. This can happen for many reasons:

1. Improperly Filled Out W-4: Though it appears to be easy, Form W-4 (Employee's Withholding Certificate) can be complicated based on your position and potential life changes.

2. Multiple sources of income: Form W-4 allows you to identify multiple sources of income and withhold.

3. Updating Form W-4: Submitting a new Form W-4 to the source of income will update your circumstances to the payroll processor or custodian. This will update the amount withheld for each source of income.

If you are self-employed or have income that is not subject to withholding, you may be required to make estimated tax payments throughout the year. Owing at the end of the year can occur if you underestimate your tax liability when making these payments. To avoid this, it's important to accurately estimate your tax liability and make timely estimated payments.

Major life changes such as a change in income, marital status, or the birth of a child can impact

your tax liability. If you don't adjust your withholding or estimated payments to account for these changes, you may end up owing more when you file your return.

Owing taxes at the end of the year can also result from not taking full advantage of available tax credits and deductions. Some taxpayers may not be aware of all the credits and deductions they are eligible for, or they may not have kept adequate records of their expenses.

If you have capital gains from investments or other sources of taxable income beyond your regular

salary, you may owe additional taxes. These types of income are often subject to different tax rates and may not have sufficient withholding. Since investment income may vary greatly by year, consulting with

your financial advisor or custodian is important. Ask about large transactions or large gains/losses being recognized. State and Local Taxes:

Remember that your federal income tax return is only part of your overall tax picture. If you live in a state or locality with income taxes, your overall tax liability may be higher, and you could owe state and local taxes in addition to federal taxes.

Taxes will be a consistent burden for the rest of your life but should not be similar to gambling. By taking a proactive approach to managing your tax liability throughout the year, you can help prevent the unpleasant surprise of owing taxes when you file your Form 1040. If you would like to schedule a consultation to better understand why you owe at the end of each year, please click the button below. We are happy to help you understand the source of your tax liabilities.

Tax season can be a daunting time for many individuals and businesses alike. Consequently, understanding the intricate details of the U.S. federal tax system is no small feat, and one aspect that often confuses taxpayers is estimated payments. In this article, we will explore the concept of estimated payments for federal tax purposes, demystify the process, and offer guidance on how to manage your tax obligations more effectively.

Estimated payments, also known as estimated taxes, are a method used by individuals and businesses to pay their federal income tax liabilities throughout the year. The U.S. tax system operates on a "pay-as-you-go" basis, meaning taxpayers are required to make payments throughout the year rather than waiting until the end of the tax year to settle their tax bill. As a result, this approach helps the government collect revenue regularly and prevents taxpayers from facing large, unexpected tax bills.

Estimated payments are typically required for the following groups:

1. W2 Employees: If you are an employee who typically owes at the end of the year or you have requested decreased withholding on your W4, you may be required to make payments to avoid penalty and interest.

2. Self-Employed Individuals: If you are self-employed, a freelancer, or a gig worker, you likely don't have taxes withheld from your income. In this case, you are responsible for making estimated tax payments.

3. Business Owners: Owners of certain types of businesses, such as sole proprietorships, partnerships, S corporations, and some LLCs, are generally required to make estimated tax payments.

4. Investors and Rental Property Owners: If you receive income from investments or rental properties and do not have sufficient taxes withheld, you may need to make payments.

5. High Earners: High-income individuals who receive a substantial amount of income not subject to withholding, such as capital gains or dividends, may also need to make payments.

Failing to make estimated tax payments when required by the IRS can result in severe penalties and interest charges. Consequently, these penalties are designed to encourage taxpayers to meet their tax obligations throughout the year rather than waiting until the end of the tax year. Here are the key penalties you may face for not making estimated payments:

Underpayment Penalty (Form 2210): This penalty is assessed when you haven't paid enough in estimated taxes by the due dates. The penalty is typically calculated on a quarterly basis. Therefore, to avoid this penalty, you must meet one of the following: a safe harbor requiring you to pay either 90% of your current year's tax liability or 100% of the previous year's tax liability (110% if your adjusted gross income exceeds $150,000 for individuals or $75,000 for married couples filing separately). Keep in mind that different rules may apply to high-income individuals along with other specialized industries.

Late Payment Penalty: If you don't make your estimated tax payments by their due dates, you may be subject to a late payment penalty. This penalty is calculated based on the amount of taxes owed and the number of days the payment is late. The IRS sets the interest rates for late payments, which can

change periodically.

Interest Charges: In addition to penalties, you may also be required to pay interest on the amount of underpaid taxes. Furthermore, the interest rate is determined by the IRS and is generally based on the federal short-term rate plus 3%. The interest rate today is significantly higher than the rates for the past decade.

Topic No. 653

Failure to File: A penalty often assessed at the same time as underpayment penalties is the Failure to File penalty. Interest is also assessed on penalties as those penalties are assessed.

While the penalty for underpayment of estimated taxes is not a fixed percentage of the underpaid amount, it is still important to be aware of the factors that can affect the penalty amount, such as the amount of underpayment, the timing of the underpayments, and the applicable interest rates.

Calculating your estimated tax payments is complex, as it depends on your income, deductions, credits, and other factors. Therefore, the simplest calculation involves estimating your total tax owed for the year and then dividing it into four equal quarterly payments.

1. Estimate your adjusted gross income.

2. Calculate your anticipated deductions and credits.

3. Determine your taxable income.

4. Apply the appropriate tax rate to your taxable income.

5. Divide your estimated annual tax liability by four to get your quarterly

payment amount.

Even though your income fluctuates throughout the year, or on a year-by-year basis, you may need to adjust your estimated taxes accordingly each year. This situation is most common for businesses trying to calculate their estimated business tax payments. In this case, having consistent bookkeeping up-to-date along with a forecast is the best way to accurately calculate your tax liability at the end of the year.

1. First Quarter: April 15

2. Second Quarter: June 15

3. Third Quarter: September 15

4. Fourth Quarter: January 15 of the following year (for the previous tax

year)

It's crucial to mark these dates on your calendar and ensure you make your payments on time. Consequently, failure to do so can result in penalties and interest.

1. Pay Online: The IRS offers an online payment system that allows you

to make payments electronically. You can use the Electronic Federal

Tax Payment System (EFTPS) or pay directly on the IRS website.

2. Mail a Check: If you prefer to pay by check, you can download Form

1040-ES from the IRS website and follow the instructions to mail your

payment.

3. Use a Tax Professional: Many tax professionals and accountants can

help you calculate your estimated payments and ensure they are

submitted on time.

Therefore estimated payments for federal tax purposes are an essential aspect of the U.S. tax system. By understanding who needs to make these payments, how they are calculated, and when they are due, you can stay on top of your tax obligations and avoid potential penalties and interest charges.

Despite the challenges of estimated tax payments, they are a proactive way to manage your tax liability and ensure you meet your obligations to the IRS. Additionally, consider working with a tax professional or using tax preparation software to streamline the process and help you accurately estimate and pay your taxes throughout the year. This proactive approach can lead to smoother tax seasons and better financial planning for the future.