Selling your home can be a major life event. It's important to understand the federal tax implications before you put your house on the market. One of the biggest concerns for homeowners is how to minimize their federal tax liability when they sell their house.

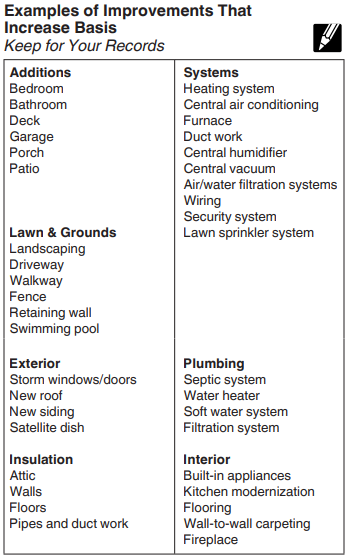

The Internal Revenue Service (IRS) plays an important role in the sale of your home. When you sell your home, you may be required to pay taxes on the capital gain. This is the difference between the sale price and your adjusted basis. (the purchase price plus any improvements you've made to the home, minus depreciation)

Minimizing your tax liability when selling your house takes careful planning and understanding of the applicable tax regulations.

Here are some key strategies to consider:

Qualify for the home sale exclusion. This exclusion allows you to exclude up to $250,000 ($500,000 for married couples filing jointly) of capital gains from the sale of your primary house from your taxable income. To qualify, most have owned and used the home as your primary home for at least two of the five years leading up to the sale.

Maximize deductions. Take advantage of allowable deductions to reduce your taxable income. These deductions may include expenses related to home improvements, selling costs, and depreciation. Keep meticulous records of all expenses to support your deductions.

Time the sale strategically. If you have other income deductions, such as charitable contributions or medical expenses, consider selling your home in a year when you can claim these deductions to further reduce your overall tax liability.

Seek professional guidance. Consult a tax professional to ensure you are maximizing tax benefits and complying with all applicable regulations. They can help you understand the nuances of the home sale exclusion, identify eligible deductions, and develop a comprehensive tax-minimization strategy.

Understand the implications of selling to family or friends. Selling your home to a family member or friend may disqualify you from certain tax benefits, such as the home sale exclusion. Carefully evaluate the tax consequences before proceeding with such a transaction.

Be mindful of selling at a loss. If you sell your home for less than you paid for it, you may not be able to deduct the loss from your taxable income. Consult a tax advisor to understand the specific rules governing loss deductions.

Consider deferred capital gains. If you defer capital gains from the sale of your home, you may eventually have to pay taxes on those gains. Evaluate the long-term tax implications of deferring gains.

By implementing these strategies and seeking professional guidance when needed, you can effectively minimize your tax liability when selling your house and maximize your financial gains.

Other Possible Deductions

In addition to the home sale exclusion, there are a number of other deductions that you may be able to claim when you sell your home. These deductions may include expenses related to selling your home, such as real estate commissions and closing costs. You may also be able to deduct certain home improvements that you made in the years leading up to the sale.

Here are some additional tips that may be helpful:

Plan ahead. The more time you have to plan, the more likely you will be able to take advantage of all of the tax breaks available to you.

Be organized. When you're selling your home, you'll need to keep track of a lot of different things. Your purchase price, home improvements, and any other expenses related to the sale are examples of this. By being organized, you'll make it easier to file your taxes and claim all of the deductions you're eligible for.

Get professional help. If you're not comfortable filing your taxes on your own, consider hiring a tax professional. A tax professional can help you understand the tax implications of selling your home. They can also develop a plan to minimize your tax liability.

If you are selling your home, it is important to report the sale on your tax return. You will need to report the sale price of your home, your adjusted basis, and any capital gains or losses that you realized from the sale. You may also need to report any deductions that you are claiming related to the sale of your home. Selling your home can be a complex process, but it doesn't have to be overwhelming. By following these tips, you can ensure that you are reporting the sale of your home to the IRS correctly and minimizing your tax liability.

Tax Disclaimer

The information provided on this website/article is for general informational purposes only and should not be construed as legal, financial, or tax advice. Every individual or business situation is unique, and tax laws and regulations can change frequently. Therefore, the content presented here may not be applicable to your specific circumstances and should be used to generate questions and conversations with your qualified tax advisor for why the content presented should or should not be used by you. It is crucial to consult with a qualified tax professional or attorney who can assess your individual or business tax situation and provide guidance tailored to your needs. Only a qualified tax expert can provide you with accurate and up-to-date advice that takes into account the latest tax laws and regulations. Any reliance you place on the information provided on this website/article is at your own risk. We make no representations or warranties, express or implied, about the completeness, timeliness, accuracy, reliability, suitability, or availability of the information contained herein.