Selling your home can be a major life event. It's important to understand the federal tax implications before you put your house on the market. One of the biggest concerns for homeowners is how to minimize their federal tax liability when they sell their house.

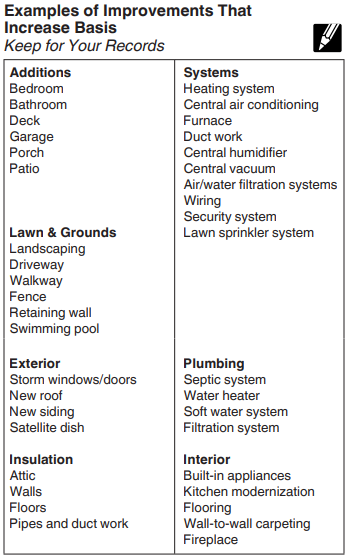

The Internal Revenue Service (IRS) plays an important role in the sale of your home. When you sell your home, you may be required to pay taxes on the capital gain. This is the difference between the sale price and your adjusted basis. (the purchase price plus any improvements you've made to the home, minus depreciation)

Minimizing your tax liability when selling your house takes careful planning and understanding of the applicable tax regulations.

By implementing these strategies and seeking professional guidance when needed, you can effectively minimize your tax liability when selling your house and maximize your financial gains.

In addition to the home sale exclusion, there are a number of other deductions that you may be able to claim when you sell your home. These deductions may include expenses related to selling your home, such as real estate commissions and closing costs. You may also be able to deduct certain home improvements that you made in the years leading up to the sale.

If you are selling your home, it is important to report the sale on your tax return. You will need to report the sale price of your home, your adjusted basis, and any capital gains or losses that you realized from the sale. You may also need to report any deductions that you are claiming related to the sale of your home. Selling your home can be a complex process, but it doesn't have to be overwhelming. By following these tips, you can ensure that you are reporting the sale of your home to the IRS correctly and minimizing your tax liability.

In the busyness of our daily lives, it's easy to view tax season as just another to-do list item. For many, that means a quick rush to file taxes without a second thought. However, there's a hidden gem in the realm of financial responsibility that often goes overlooked: the tax return review. In this article, we'll explore why a tax return review is crucial for your financial well-being. Additionally, we will look at how it can help you maximize your financial potential. The best part of our services is that you do not need to switch your current tax preparer.

We're focused on providing information so that you can ask good questions and work towards getting an accurate tax return. Most tax preparers appreciate good questions as it also reduces their own liability if the tax return is done properly. The most important thing to understand, it is your responsibility as the taxpayer to have an accurate tax return. Tax preparers hold very little liability and it is the taxpayer’s responsibility to understand the tax return being filed.

Before delving into the importance of a tax return review, let's clarify what it entails. A tax return review involves a thorough look at your filed tax return by a Certified Public Accountant (CPA). This process goes beyond a cursory glance to identify potential errors, missed deductions, or opportunities for tax savings. It is intended to provide opportunities to minimize tax liabilities. It will also educate and inform you on your tax return, and reduce tax noncompliance where hidden errors are occurring.

The most important reason for getting your tax return reviewed is to educate yourself on what the tax return says. Through a quick explanation of what the tax return says, you can compare it to what you already know about your business. This comparison helps identify errors immediately but also helps reduce errors through your ability to understand the key points of a tax return.

Another primary reason for having your tax return reviewed is to catch any errors or omissions in your

filing. Even the most diligent taxpayers can make mistakes, and these errors can lead to costly penalties or audits. A professional review can help identify and rectify these issues before they escalate. Hidden mistakes from unintentional errors and omissions can bankrupt a company unexpectedly. Our focus is on improving your business’ financial health.

Tax laws are complex, and they change regularly. A tax professional is well-versed in these laws and can ensure that you are taking advantage of all available deductions and credits. This can result in significant tax savings that you might have otherwise missed.

Tax return reviews are not just about finding deductions; they are also about optimizing your overall tax

strategy. A tax professional can help structure your finances in a way that minimizes your tax liability, ensuring that you keep more of your hard-earned money.

IRS Tax audits can be stressful and time-consuming. By having your tax return reviewed, you reduce the risk of incurring a tax liability during the IRS audit due to inaccuracies or inconsistencies. Additionally, if you do face an audit, having a professionally reviewed tax return can help. The review can create and advise towards valuable documentation and support which may be forgotten later.

A tax return review can be a valuable part of your overall tax planning. It provides insights into your future tax health, highlights areas for improvement, and helps you make informed decisions about your future financial goals. Tax Planning is a crucial component in paying the least amount of taxes over your entire life. There are situations where paying the least amount of tax today, creates a large tax liability in the future which can be identified.

In the world of personal tax and finance, a tax return review is a powerful tool that should be regularly utilized. It serves as a safeguard against costly mistakes, a catalyst for maximizing your tax benefits, and a means of ensuring compliance with tax regulations. By investing in a tax return review, you not only protect your financial well-being but also pave the way for a more secure and prosperous financial future. Don't let tax season pass you by without taking advantage of this opportunity to achieve peace of mind and financial success. Trust in the expertise of professionals who can provide a thorough Tax Return Review, and watch as your financial potential unfolds before you.

As tax season approaches, one of the most critical decisions you'll make is choosing the right tax preparer who can navigate the complex world of taxation while ensuring your financial well-being. Not all tax professionals are created equal and attention to detail is the largest quality to the accuracy of your tax preparer. To help you make an informed choice, we've compiled a guide on essential certifications and qualifications you should be looking for when finding and qualifying a tax preparer.

Anyone with an IRS Preparer Tax Identification Number (PTIN) is authorized to prepare federal tax returns. To obtain a Preparer Tax Identification Number (PTIN), individuals must go through a quick registration process with the IRS. However, the qualifications necessary to identify yourself as a tax preparer are very low and there are no educational requirements.

Based on demand and the ability to easily set up a business, many seasonal tax firms pop up around Florida. Seasonal tax preparers are often hired temporarily during tax season to handle the influx of returns. They may not always possess the necessary credentials, making them more susceptible to becoming ghost preparers. It's crucial for taxpayers to exercise caution when seeking assistance from such preparers. Even though some seasonal preparers may be legitimate and have the requisite skills, it's essential to verify their qualifications. You should ask for their PTIN, and ensure they are associated with a reputable tax preparation service or organization. Being diligent in your selection process can help you avoid the potential pitfalls associated with ghost preparers and ensure that your tax return is handled accurately and ethically.

Typically, looking for an accounting firm is a good way to avoid unqualified tax preparers. Each state also has their own requirements for marketing and the naming of an accounting firm. In Texas, the law does not allow you to identify as an Accountant in your name unless you hold a Certified Public Accountant License. In Florida, there are very few rules when starting an accounting firm and there are very few restrictions on what you can name a business. Thus, a person with no qualification can start an accounting firm tomorrow within Florida.

If you are specifically looking for a certified individual to perform your work. Looking for a business with “CPAs” within its name is important. CPA firms must have the majority of their ownership owned by a CPA. The reason why the “s” is so important is that it indicates multiple CPAs are involved within the ownership. Firms with multiple certified individuals perform better as the firm is less likely to rely on one person to make decisions. This increases the ability of the firm to prepare an accurate return and also typically reflects a larger amount of knowledge in the firm. If you do not require a CPA firm to perform your work, it is much harder to qualify a preparer for your tax return through the business’ name.

There are many important qualities to think about when choosing a tax preparer. The most important one is whether the preparer has the ability to defend their work in front of the IRS. You will find this quality important if you receive an IRS Audit letter in the future. If your preparer is not able to defend each step of an IRS Audit, you will need to involve additional individuals which may cost substantially more in your defense.

Enrolled Agents are tax experts licensed by the IRS. They must pass a three-part exam, demonstrating proficiency in federal tax planning, individual and business tax return preparation, and representation. EAs are required to complete 72 hours of continuing education every three years. Enrolled Agents are certified in Tax services which includes portions of accounting. The certification’s tests focus on tax compliance and tax return preparation for individuals and businesses. Typical services performed by Enrolled Agents include tax preparation, tax planning, IRS Representation, and many other tax related services.

CPAs are licensed by state boards of accountancy. They have passed the Uniform CPA Examination, which is a 4 part exam. CPAs have taken 150 hours of college credit, much of which must be high level accounting courses, and typically have a Bachelor’s degree. CPAs also must meet experience and ethical requirements and engage in ongoing continuing education to maintain their CPA license. The CPA license is intended to be the most broad and prestigious license in Accounting.

The Uniform CPA Examination is known to be one of the hardest exams to pass. By identifying a CPA as your preferred tax preparer certification, you are guaranteeing a well-rounded accountant is preparing your return. Each part of the 4 part exam has a pass rate around 50% along with an average study period of over 12 months. Therefore, utilizing a CPA for your tax preparation is considered to be the safest option if you are qualifying a tax preparer by their certification.

In regards to tax preparation, not every CPA has the knowledge to perform tax preparation well. Qualifying that the CPA has a focus on tax preparation and tax strategies is a good idea when looking for a tax preparer. Typical services performed by a CPA include all tax services, accounting services, advisory and audit services, along with almost every other service in accounting. Just keep in mind that CPAs should not identify as being good at all services and typically have a specialization such as tax return preparation.

Attorneys are licensed by state courts or their designees, such as the state bar. They have earned a degree in law and passed a bar exam. Attorneys are held to high ethical standards and must participate in ongoing continuing education. Most attorneys performing tax preparation are tax attorneys. Tax attorneys typically have extensive and specialized knowledge in accounting and tax.

Tax preparers without the above-mentioned credentials, have limited practice rights. They can only represent clients before specific IRS employees but not in appeals or collection issues. These preparers include:

To assist taxpayers in determining the credentials and qualifications of tax professionals, the IRS maintains a public directory. This searchable database includes the names, locations, and credentials of attorneys, CPAs, enrolled agents, enrolled retirement plan agents, and enrolled actuaries with valid PTINs, as well as Annual Filing Season Program Record of Completion recipients for the current tax year.

It is crucial to ensure that your tax preparer holds the necessary credentials and qualifications to handle your financial affairs effectively. For this reason, always verify that your tax preparer has an IRS-issued PTIN, which is required by law for anyone who prepares tax returns for compensation. When selecting a tax professional, inquire about their education, training, and experience to make an informed choice. Your financial well-being depends on it, so choose wisely and with confidence.